The summary financial statements were prepared in compliance with Articles 19 and 20 of the BOIP’s financial regulations.

Bonds, shares and other investments are stated at fair value. The realised and unrealised results are recognised in the income statement.

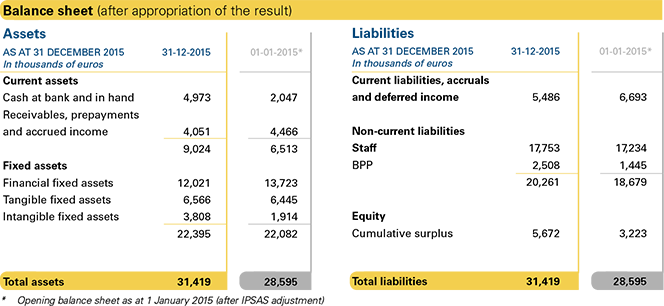

The tangible and intangible fixed assets are stated at cost or on the basis of the costs incurred, less accumulated depreciation and, if applicable, less impairments.

Current liabilities mainly consist of deferred income (payments for services not yet rendered).

Non-current liabilities mainly consist of liabilities connected with staff rules which are required by the IPSAS to be accounted for under liabilities. The pensions, the part-time working scheme for older staff (PAS scheme) and pension bonus debt positions are new. The debt resulting from healthcare costs after retirement is a consequence of the Headquarters Agreement.

In addition to the cumulatively withheld operating results, the cumulative surplus also reflects the changes in the non-current liabilities incorporated directly via the equity. In 2015, that involved the adjustment of the interest rate for the calculation of non-current liabilities for staff from 2% to 2.5%. In the case of the liabilities for pensions and healthcare costs after retirement this resulted in a release of €1,527,000.